Mejappz

Elite Member

- Joined

- Dec 16, 2005

- Professional Status

- Certified Residential Appraiser

- State

- Florida

I haven't read it yet (it's 47 pages), but I predicted this years ago. Cheap and fast options often come with consequences. I'll be curious to see if there's any mention of AMCs or lenders—after all, they’re responsible for ordering the appraisals.

www.fhfa.gov

www.fhfa.gov

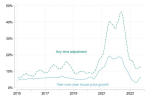

Mortgage appraisal accuracy became a major concern following the global financial crisis in the late 2000s. Legislative standards and industry guidance have adjusted professional practices to improve inefficiencies and inequities. Nonetheless, systematic misvaluation continues to be documented for single-family residential homes, which creates problems when appraisals are used by financial lenders to gauge potential risk and an asset’s worth. Real estate prices have been appreciating continuously over the last dozen years, which means comparable sales and benchmark indices merit revisions to reflect fair market conditions, but it only happens for around 10% of properties. We sample from a uniform appraisal database of over 45 million records from “subject” single-family properties and 228 million records from “comparable” homes covering the entire United States from 2015 through 2023. This paper asks whether time adjustments are made, if they improve fair market measurements, and whether they fix neighborhood appraisal disparities. Results show these readily available corrections are underutilized, too small, applied less frequently in minority areas, and cure half of initial underappraisals. The limited usage of time adjustment accounts for as much as 67% of the underappraisal bias in Black neighborhoods and 49% of the disparity in Hispanic neighborhoods.

Working Paper 24-07: Underappraisal Disparities and Time Adjustments to Comparable Sales Prices in Mortgage Appraisals | FEDERAL HOUSING FINANCE AGENCY

Author: William M. Doerner, Scott Susin

Mortgage appraisal accuracy became a major concern following the global financial crisis in the late 2000s. Legislative standards and industry guidance have adjusted professional practices to improve inefficiencies and inequities. Nonetheless, systematic misvaluation continues to be documented for single-family residential homes, which creates problems when appraisals are used by financial lenders to gauge potential risk and an asset’s worth. Real estate prices have been appreciating continuously over the last dozen years, which means comparable sales and benchmark indices merit revisions to reflect fair market conditions, but it only happens for around 10% of properties. We sample from a uniform appraisal database of over 45 million records from “subject” single-family properties and 228 million records from “comparable” homes covering the entire United States from 2015 through 2023. This paper asks whether time adjustments are made, if they improve fair market measurements, and whether they fix neighborhood appraisal disparities. Results show these readily available corrections are underutilized, too small, applied less frequently in minority areas, and cure half of initial underappraisals. The limited usage of time adjustment accounts for as much as 67% of the underappraisal bias in Black neighborhoods and 49% of the disparity in Hispanic neighborhoods.